Picking an investment account in Gscfinanceville feels like trying to read a menu in another language. You stare at the words. You nod along.

But you’re not sure what any of it actually does for you.

Which one helps you buy your first home? Which one gets you closer to retiring early? Which one just eats fees and gives you nothing back?

I’ve opened all of them. Some worked. Some were a waste of time (and money).

This isn’t theory. It’s what I learned after losing money, overpaying, and finally getting it right.

You don’t need ten accounts. You need one that fits your actual life. Not some generic checklist.

We’ll cut through the jargon. No fluff. No hype.

Just clear differences between the real options in Gscfinanceville.

You’ll know exactly what each account does, who it’s really for, and where yours fits.

By the end, you’ll know Which Investment Account to Open Gscfinanceville (and) why it’s the right call for you.

Not someone else’s goals. Not some textbook example. Yours.

You’ll walk away ready to open it. Or walk away from the wrong one. Either way (you) win.

Why Are You Investing?

I start every conversation about money with one question: why do you want to invest? Not what you hope happens. Not what your cousin’s friend did.

Why you.

You might be saving for retirement. Or a house down payment. Or your kid’s college tuition.

Or just tired of watching your cash lose value in a savings account. All valid. None are wrong.

But here’s what trips people up: your goal decides your timeline. Short-term (under 5 years)? You can’t afford big swings.

Medium-term (5. 15 years)? You’ve got some room (but) not much. Long-term (15+ years)?

That’s where stocks and time do real work.

Which Investment Account to Open Gscfinanceville depends entirely on that answer. Not on what’s trending. Not on what your broker pushes.

On your why.

A short-term goal needs safety. Maybe a high-yield savings account or short-term CDs. Retirement?

A Roth IRA or 401(k) makes more sense. You wouldn’t park money for a house in the same place you’d stash retirement cash. Would you?

Go look at Which Investment Account to Open Gscfinanceville (but) only after you write down your goal and timeline first. Seriously. Do it now.

Retirement Accounts That Actually Work

I opened my first 401(k) the day I got my first real paycheck. No seminar. No spreadsheet.

Just clicked “enroll” because my boss said, “They’ll match half up to 6%.”

That match is free money.

You leave it on the table, you’re paying yourself less.

IRAs are different. You open them yourself. No employer needed.

Just a bank or brokerage and five minutes online.

Traditional IRA? You might deduct your contribution now. But you pay taxes later.

When you pull money out in retirement.

Roth IRA? You pay taxes now. Then every dollar you pull out later (growth) included (is) tax-free.

So which makes sense? If you’re making $45k and expect $90k in retirement? Roth.

If you’re at $120k now and plan to retire early with low income? Traditional.

Don’t overthink the “right” choice.

Most people should do some of both.

2024 contribution limits: $23,000 for 401(k)s. $7,000 for IRAs. (Yes, you can do both (and) yes, you should if you can.)

Which Investment Account to Open Gscfinanceville depends on your paycheck, your tax bracket, and whether your employer matches. Not your astrological sign. Not your friend’s cousin’s broker.

Start with the 401(k) match. Then add a Roth IRA. Then keep going.

You don’t need perfection.

You need action.

And no (“someday”) doesn’t count as a date.

Brokerage Accounts: Your Money, No Rules

I open brokerage accounts when I want full control. No retirement deadlines. No contribution caps.

These are taxable accounts. You pay taxes on profits when you sell. Simple.

Not free (but) predictable.

I dump in $500 or $50,000. I pull it out next week or in ten years. The IRS doesn’t care.

Stocks? Bonds? ETFs?

Mutual funds? All allowed. No gatekeepers.

Need a house down payment in three years? A brokerage account works. Building long-term wealth?

No permission slips.

It works too.

But here’s the catch: no tax breaks like with IRAs or 401(k)s.

You’re trading flexibility for upfront tax savings.

Which Investment Account to Open Gscfinanceville depends on your timeline and goals. If you’re unsure where to start (or) whether a brokerage account fits your plan (I’d) talk to someone who’s done this before. learn more

Retirement accounts lock money up. Brokerage accounts don’t. That’s not better or worse.

Just different.

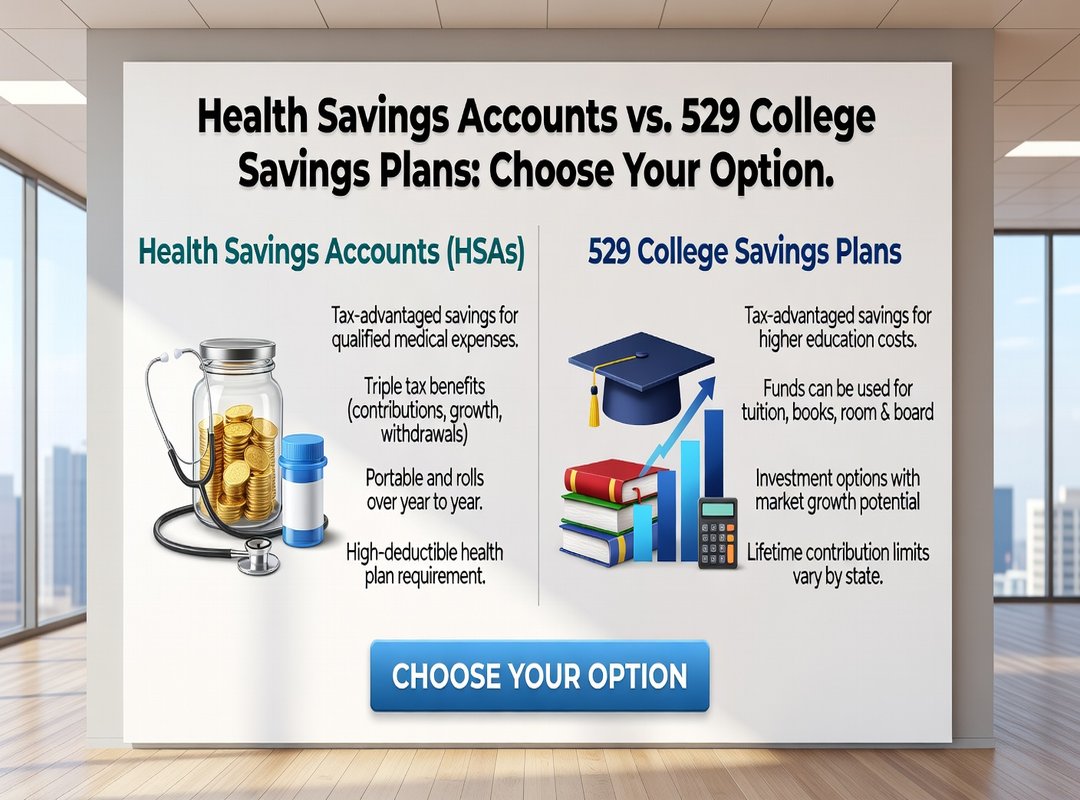

HSAs and 529s: Pick One. Not Both.

I open an HSA before a 529. Every time.

HSAs are the only accounts with triple tax advantage. Tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical bills. (Yes, even tampons and insulin count.)

You need a high-deductible health plan to qualify. If you have one. And most people with employer plans do.

It’s free money. I treat mine like a stealth retirement account after 65. No penalties.

Just smart spending.

529 plans? Solid for college savings. Tax-free growth.

Tax-free withdrawals for tuition, books, even some K-12 costs in certain states. But they’re rigid. Use it for non-education expenses?

You pay taxes and a 10% penalty.

So who wins? If your kid’s not born yet. Or you’re still paying off student loans.

Which Investment Account to Open Gscfinanceville? Start with the HSA. Then maybe the 529.

Skip the 529. Fund the HSA first. Your future self will thank you when you’re 68 and using that money for cataract surgery.

Not the other way around.

You already know your health costs are rising. Are you really betting your kid will go to college and stay in-state?

What to Do Next in Gscfinanceville

Which Investment Account to Open Gscfinanceville?

It depends on what you want, how soon you need it, and how much tax paperwork you’ll actually handle.

I started with $500 in a Roth IRA. You could too. Don’t wait for “perfect.” Start small.

Learn as you go.

Your goals matter more than the account name. Retire in 30 years? Roth IRA.

Save for a house in 5? Brokerage. Paying college next year? 529.

Timeline changes everything. Taxes? If you hate forms, avoid accounts that create them.

Talk to someone local (or) use an online broker that serves Gscfinanceville. You don’t need a fancy title to get good advice. Just ask questions.

Where can i find financial advice gscfinanceville. That page has real names and no sales pitch.

Your First Move Starts Now

I opened my first account with zero confidence. You don’t need confidence. You need clarity.

You now know the difference between retirement, general, and specialized accounts.

That’s not trivia (that’s) use.

Choosing wrong costs time. Choosing right moves you forward faster.

Which Investment Account to Open Gscfinanceville?

It depends on your goal (not) someone else’s template.

What are you saving for? A home? Retirement?

A business?

Review your goal. Match it to the account. Then open it.

Don’t wait for “someday.”

Someday is a myth.

Open the account that fits your life (today.) Not next week. Not after research. Today.

Go do it.

Creative Director & Lifestyle Content Lead

Lirithyn Dusklance oversees the visual identity and lifestyle direction of FMB MotoTune. Her work focuses on blending motorcycle culture with modern design trends, rider apparel, travel inspiration, and everyday gear recommendations. She has a sharp eye for aesthetics and storytelling, helping the platform maintain a bold yet approachable style. Lirithyn contributes heavily to branded campaigns, feature layouts, and audience engagement strategies that resonate with both experienced riders and newcomers. Her creative approach ensures that the platform remains visually dynamic while staying informative and authentic. Through her leadership, FMB MotoTune continues to strengthen its connection with the wider riding lifestyle community.

Creative Director & Lifestyle Content Lead

Lirithyn Dusklance oversees the visual identity and lifestyle direction of FMB MotoTune. Her work focuses on blending motorcycle culture with modern design trends, rider apparel, travel inspiration, and everyday gear recommendations. She has a sharp eye for aesthetics and storytelling, helping the platform maintain a bold yet approachable style. Lirithyn contributes heavily to branded campaigns, feature layouts, and audience engagement strategies that resonate with both experienced riders and newcomers. Her creative approach ensures that the platform remains visually dynamic while staying informative and authentic. Through her leadership, FMB MotoTune continues to strengthen its connection with the wider riding lifestyle community.